The Perfect Home Could Be the One You Perfect After Buying

There’s no denying mortgage rates and home prices are higher now than they were last year and that’s impacting what you can afford. At the same time, there are still fewer homes available for sale than the norm. These are two of the biggest hurdles buyers are facing today. But there are ways to overcome these things and still make your dream of homeownership a reality.

As you set out to make a purchase this season, you’ll want to be strategic. This includes taking a close look at your wish list and considering what features you really need in your next home versus which ones are nice-to-have. This will help you avoid overextending your budget or limiting your pool of options too much because you’re searching for that perfect home.

Danielle Hale, Chief Economist at Realtor.com, explains:

“The key to making a good decision in this challenging housing market is to be laser focused on what you need now and in the years ahead, . . . Another key point is to avoid stretching your budget, as tempting as it may be . . .”

To help identify what you truly need, make a list of all the features you’ll want to see. From there, work to break those features into categories. Here’s a great way to organize your list:

- Must-Haves – If a house doesn’t have these features, it won’t work for you and your lifestyle (examples: distance from work or loved ones, number of bedrooms/bathrooms, etc.).

- Nice-To-Haves – These are features you’d love to have but can live without. Nice-to-haves aren’t dealbreakers, but if you find a home that hits all the must-haves and some of these, it’s a contender (examples: a second home office, a garage, etc.).

- Dream State – This is where you can really think big. Again, these aren’t features you’ll need, but if you find a home in your budget that has all the must-haves, most of the nice-to-haves, and any of these, it’s a clear winner (examples: a pool, multiple walk-in closets, etc.).

If you’re only willing to tour homes that have all of your dream features, you may be cutting down your options too much and making it harder on yourself (and your budget) than necessary.

While you’d love to have granite countertops or a pool in the backyard, those are both things you could potentially add after you move. Instead, it may be best to focus on finding the things that you can’t change (like location or a certain number of rooms). Then, you can upgrade or add some of the other features or finishes you want later on.

Sometimes the perfect home is the one you perfect after buying it.

Once you’ve categorized your list in a way that works for you, discuss your top priorities with your real estate agent. They’ll be able to help you refine the list further, coach you through the best way to stick to it, and find a home in your area that meets your top needs.

Bottom Line

With the current affordability challenges and limited housing supply, you’ll want to be strategic so you can find a home that meets your needs while staying within your budget. Connect with a real estate agent who can help make that possible.

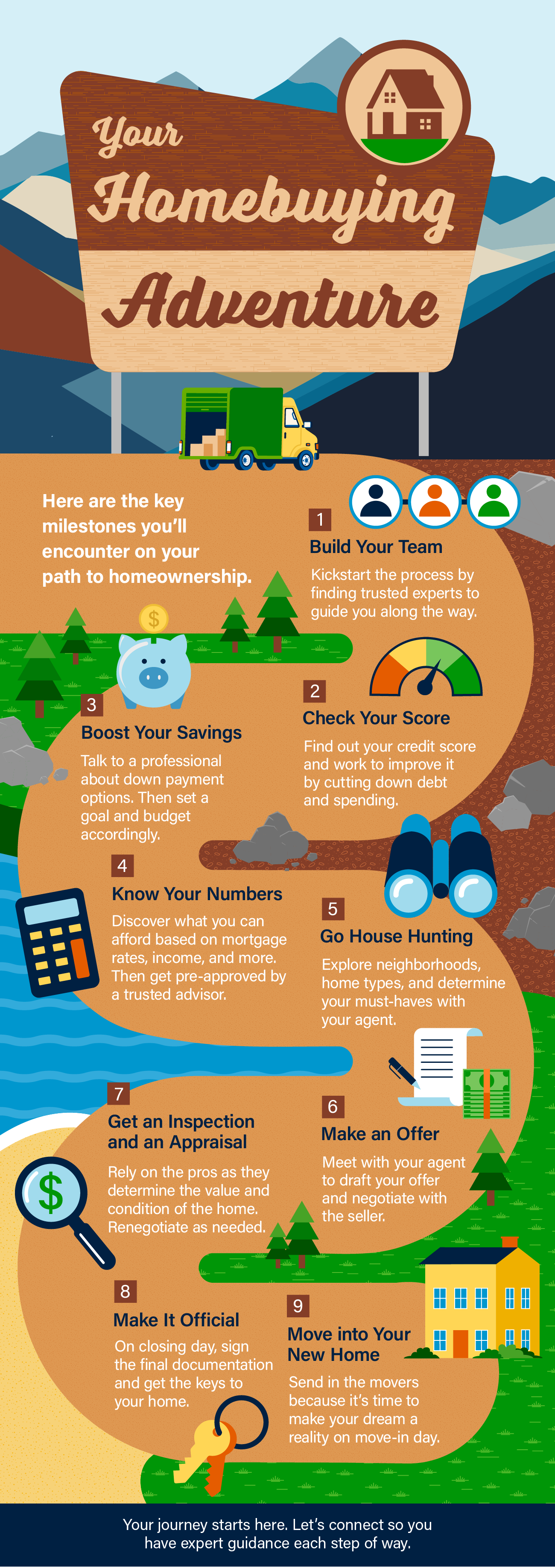

![Your Homebuying Adventure [INFOGRAPHIC] Simplifying The Market](https://allavenuerealty.com/wp-content/uploads/2023/12/Your-Homebuying-Adventure-KCM-Share.png)

![VA Loans Help Heroes Achieve Homeownership [INFOGRAPHIC] Simplifying The Market](https://allavenuerealty.com/wp-content/uploads/2023/11/VA-Loans-Help-Heroes-Achieve-Homeownership-KCM-Share.png)

Follow Us!